What to Prioritize: Debt Payoff or Saving?

This post may contain affiliate links. Check out my Disclosure Policy for more information. This is a huge conversation in the personal finance world and one that really has to be personal when it comes down to it. If you’re a Dave Ramsey follower, then…

A New Debt Payoff Strategy

This post may contain affiliate links. Check out my Disclosure Policy for more information. When I first came to the realization that I had $201k in student loan debt, I immediately hit the Internet to learn how I could manage this absurd amount of debt…

How Student Loans Impacted my Credit

When I graduated grad school in 2015 I had a plan in place to pay off my $200k in student loans. I had a teaching job lined up and planned to find some extra tutoring jobs to increase my income. I had just started really…

Debt Snowball or Avalanche?

This post may contain affiliate links. Check out my Disclosure Policy for more information. This is something I really struggled with when I began my journey to financial freedom. When I first began I was really into Dave Ramsey and using his baby steps. It’s…

Using Gift Cards to Get Through the Hard Months

When I began this debt payoff journey I was $200k in student loan debt, just starting my first year teaching, moving back home with my parents, and had no idea how I was going to manage this whole thing. I had a plan, I had…

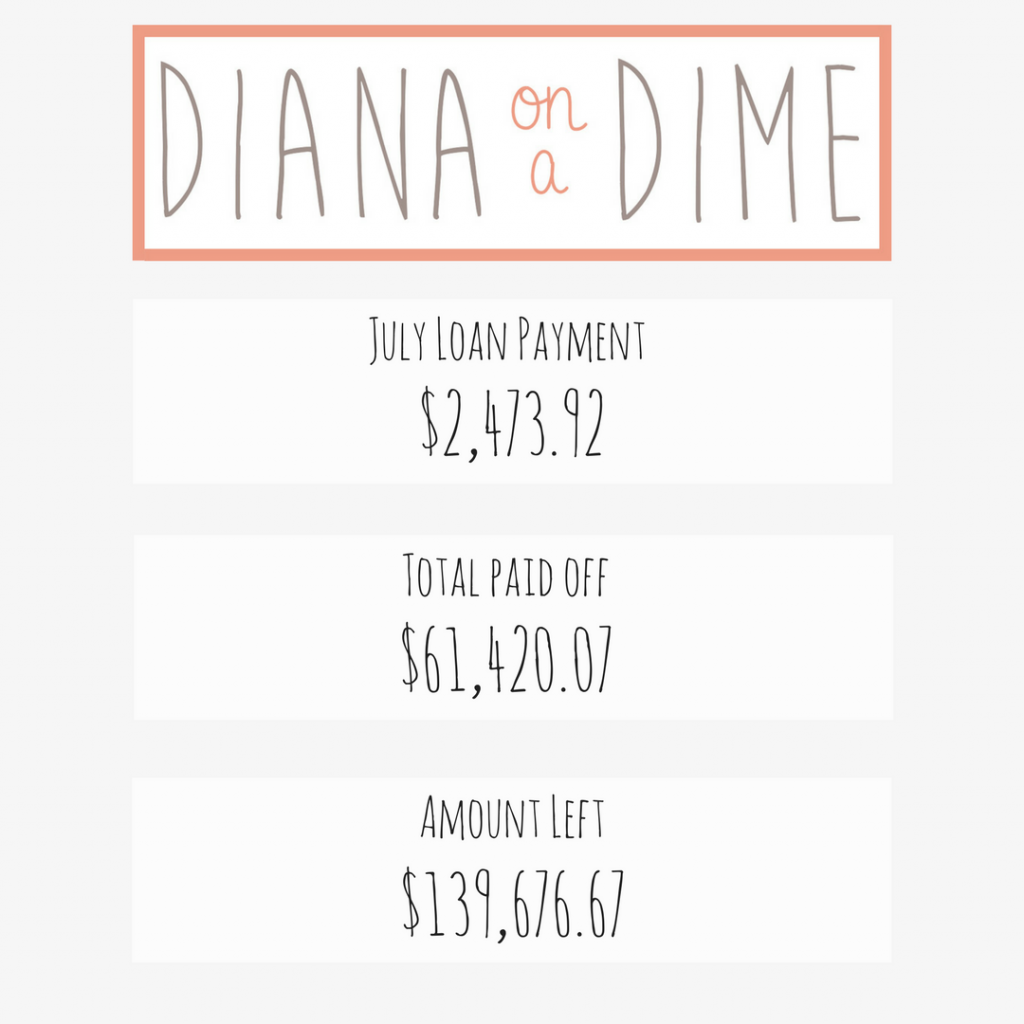

July Debt Payoff

I started my debt payoff journey in November 2015 officially. That’s when my student loans officially went into repayment and I started throwing all of my money at my debt in order to pay it off as soon as possible. Since then, I’ve made many…

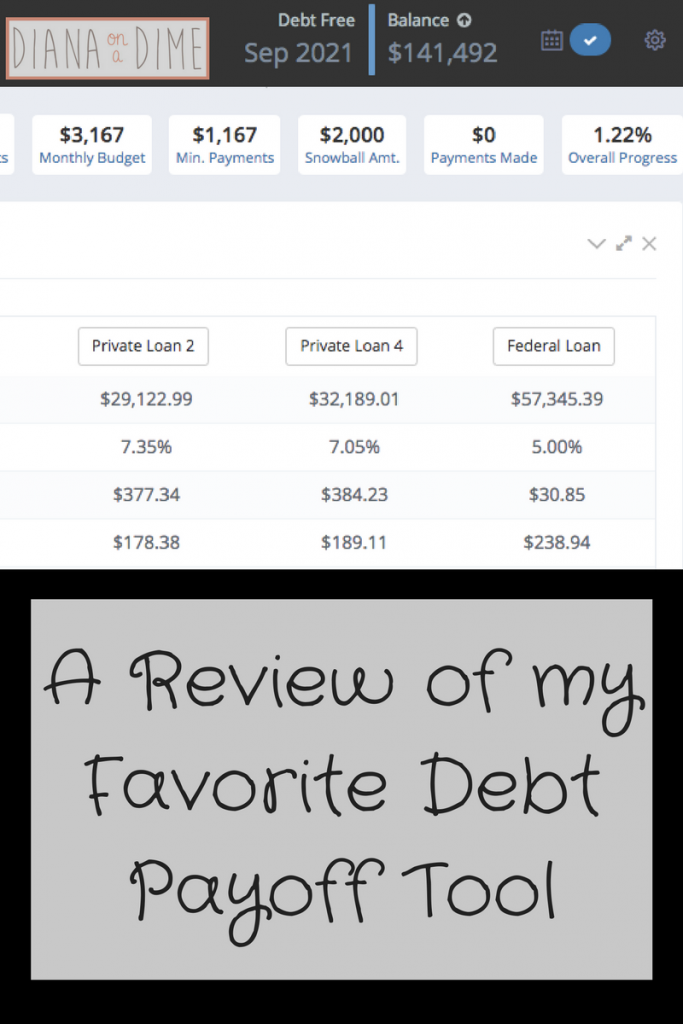

A Review of my Favorite Debt Payoff Tool

This post may contain affiliate links. Check out my Disclosure Policy for more information. Back in November of 2016 my debt payoff world came crashing down around me. My favorite debt payoff tool, ReadyForZero, was no longer going to be offering their tool. This tool…