Why Tax Deductions Shouldn’t Change Your Debt Free Journey

This post may contain affiliate links. Check out my Disclosure Policy for more information.

This time of year everyone is figuring out their taxes, filing their tax returns, making sure they get all of their tax deductions, and waiting on their tax refunds. It comes with this time of year. There is a huge personal preference to get a large refund or a small refund. I outlined why I plan to make myself get a smaller refund, but I understand why some people like a larger refund.

Currently, I get a larger refund because when I originally did my paperwork at work, I had no idea what I was doing. If I’m being totally honest, I’ve just been too lazy to change it! I plan to change it when I get a new job though.

A lot of times people get wrapped up in the tax deductions and it can be overwhelming. Lately I’ve been getting asked a lot about my debt free journey, especially by friends and family. Most of the comments I’m getting are surrounding my student loan tax deduction and not getting it when I pay off my student loans.

I try really hard not to eye roll at this, but it can be very difficult. Yes, I’ll lose my tax deduction when they are paid off, but I’ll get to keep all of that money. My friend shared this article with me that does a wonderful job explaining the math behind this, if you’re into that kinda thing like me!

Why Tax Deductions Don’t Matter

Okay, that’s being a bit dramatic. But, it isn’t exactly wrong. Yes, tax deductions are nice, but they shouldn’t dictate how you manage your finances. You should never do something solely because you’ll get a tax deduction for it, or it will lower your taxable income.

If your money move that you are making adds something else to your financial picture, then absolutely go for it! But, I wouldn’t make a move solely because you get a tax deduction. For example, I’ve literally heard people say they don’t want a higher income because it will push them into a higher tax bracket. That’s insane!!!! Taxes and tax deductions should not dictate your money moves, keep them in mind, but don’t let it sway you this much.

Let’s go back to my student loan interest tax deduction and losing that tax deduction once I’m debt free. The tax deduction would lower my taxable income by $2,500, but I’ll then be able to pocket and invest the $40k a year I’m currently paying towards my loans. Even if I just put it in a high yield savings account, that money would give me a nice return each year.

What you should do instead.

Pay off those pesky student loans! Put that money back into your budget because student loans are evil! I outlined why they are and how blind student loan payments will cause you to pay so much more on them, here. I encourage you to sit down, track your expenses, get that zero based budget going. Send all of your extra money to debt, after you have your emergency fund, and get those things out of your life for good!

If you need help with this, comment below, I love helping people get their budget set up and be sure to get my Google sheets template to help you get started with your own budget.

Don’t fall into the tax deduction trap.

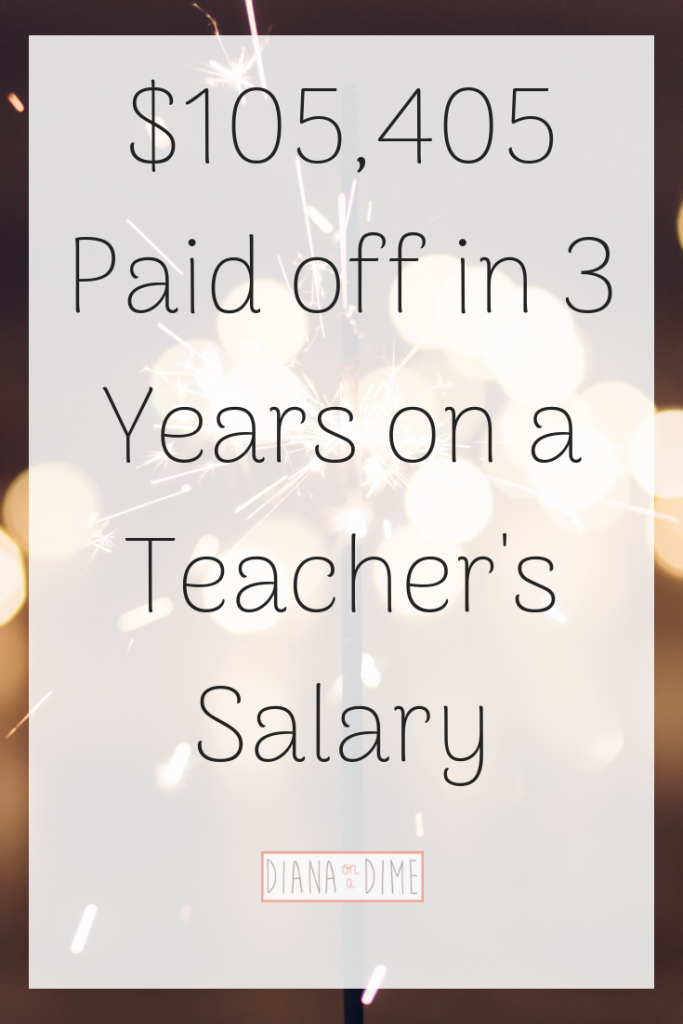

It can be easy to listen to others when they are talking about finances. Don’t be afraid to be a little weird! If I listened to the vast majority of people, I’d still be drowning in $201k of student loans, instead of only $85k (HA!). But in all seriousness, the long term benefit of not having student loans definitely outweighs the small tax deduction I’d get every year, or not if my income increases. So, let’s get moving on freeing ourselves of student loans! I’d love to hear your experiences, have people told you not to pay off your student loans for the tax deduction?

{kind=link}

{kind=link}

{kind=link}

{kind=link}